Every member of community bank leadership is searching for an AI use case in banking worth bringing to the board, but most folks don’t know what’s real and what’s just buzz. Especially in lending. There’s a lot of noise about automation and personalization, but very little about what actually helps

AI banking applications

14 posts

AI in financial institutions isn’t some far-off fantasy cooked up by Silicon Valley. It’s already shaping how money moves, how risk is managed, and how decisions get made, quietly and behind the scenes. For CFOs in community banks, that shift is no longer optional. Budgets are tight, regulations are brutal,

Corporate treasury used to be a backstage crew role, quietly keeping liquidity flowing and making sure the business could fund its plans. But the rise of AI in banking and finance has dragged treasury into the spotlight, especially when it comes to risk. Suddenly, board members are expected to understand

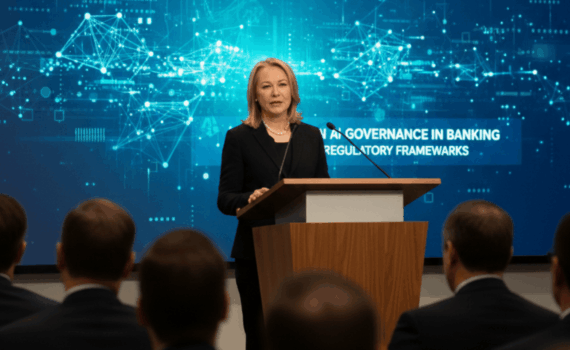

AI is picking up speed inside banks, but governance isn’t keeping pace. That’s the tension Lisa Pent is tackling at the IBANYS Regulatory Compliance Update on February 3rd. Banks are trying to push forward with smarter tools and automation, while examiners are asking sharper questions about ownership, oversight, and monitoring.

AI Execution in Mid-Tier Banking is reshaping how regional institutions strengthen workflows, improve decisions, and advance their operational capabilities. Banks in the $10 billion to $250 billion range are already moving through modernization. Many have active AI initiatives in lending efficiency, fraud detection, document intelligence, and operational review. Leaders understand

Old banking cores weren’t built for AI in banking. They weren’t built for real-time anything, honestly. And yet, they’re still the default under the hood of thousands of banks trying to keep up in 2026. The result? Slow rollouts, patchwork integrations, and a whole lot of duct tape holding together

AI use cases for community banking are starting to look a lot less like Silicon Valley wishlists and a lot more like real tools solving gritty, local problems. Picture this: a small-town branch in Iowa, a desktop monitor humming behind the teller counter, the smell of fresh coffee wafting from

Use Cases for AI in Community Banking are shifting fast from idea to real-life tools that actually do the work. Picture a small bank in Ohio. The morning sun hits the teller windows, the printer hums, and a branch manager scans the weekly performance report, already wondering how much time

AI use cases for community banking are evolving fast, and they’re not all about cost-cutting or fraud flags. One of the most surprising things is how personal this new tech can feel, especially in small, high-trust markets. Picture a small-town bank in Missouri. The sun’s hitting the brick façade, the

Community banks should lead with AI to stay relevant, competitive, and connected in a rapidly changing financial landscape. That sentence might feel bold. But it captures a truth that’s becoming more urgent by the day. The world of finance is evolving fast. Customer expectations have shifted. Compliance demands are mounting.

There has been a recent shift away from SaaS into something called “Services-as-Software” which feels way more in tune with the way we want to do business in an increasingly digital world. Community bankers have always faced unique challenges when it comes to balancing legacy systems, customer service, and the

In the world of community bank fintech, progress often feels like a tightrope walk between innovation and compliance, vision and practicality. But every now and then, the right pieces come together to make real transformation possible. That’s exactly what happened when PentEdge forged a groundbreaking partnership with Techjays, Barry N.