Artificial intelligence in digital banking is changing how community banks show up for their customers. It’s not just about faster apps or slicker websites. It’s reshaping the heart of how banks understand people, handle risk, and build trust in a world that expects everything now.

Community banks don’t always have the budgets or tech teams of national giants. But they do have something those bigger players often lack: deep roots in local neighborhoods and strong relationships with customers. With the right AI tools, they can blend old-school trust with new-school efficiency and stay in the game as banking goes fully digital.

This shift isn’t optional anymore. More folks are skipping branches and doing it all on their phones. That includes opening accounts, moving money, applying for loans, even disputing charges. If a bank can’t keep up, customers won’t wait around.

TL;DR

- What smart personalization actually looks like in a digital bank

- Why predictive analytics is a game changer for small banks

- How AI fights fraud without slowing things down

- What it takes to power 24/7 chat without hiring a night shift

- Where community bankers should start before jumping in

Smart personalization is the new customer service

AI is helping banks know their customers better than ever. This isn’t just about knowing someone’s name or balance. Smart systems can spot patterns in spending, saving, and borrowing to predict what a customer might need next.

For example, if someone’s paycheck comes in every two weeks and they tend to pay off their credit card right after, the system might offer a temporary credit increase during holidays. Or if a small business account has a cash flow dip every September, the bank could flag that early and suggest short-term funding options.

Personalization like this turns digital banking into something that feels human. Customers feel seen without needing to walk into a branch. That kind of experience builds loyalty and makes it harder for them to switch banks.

Banks that do this well use customer data in real time. They rely on machine learning models that keep getting better as more data flows in. This doesn’t just help with marketing. It helps people make better financial decisions, too.

Privacy still matters. People need to know their information is safe and being used to help, not just to sell. Transparent policies and clear opt-ins go a long way here. The best systems give control back to the user, showing them how their data is used and what they can do with it.

Predictive analytics helps banks stay one step ahead

Artificial intelligence in digital banking gives community banks a tool that used to be out of reach: serious forecasting power. Predictive analytics looks at past behavior and future possibilities. It helps banks spot who’s likely to default, who might need a loan, or who’s about to close an account.

Instead of reacting to problems, banks can prevent them. A flagged transaction pattern might show that a customer is having trouble making ends meet. That could lead to a proactive offer of financial coaching or a temporary adjustment in payment terms.

It’s not just about customers, either. AI can look at market trends and regulatory changes to help banks prepare for shifts in interest rates, inflation, or loan demand. This gives community banks a better shot at competing with larger institutions.

Small banks can use third-party platforms to get started. They don’t have to build models from scratch. What matters is knowing what questions to ask and using the data they already have to start answering them.

Good predictions rely on clean data. That means having systems in place to pull info from across departments and making sure it’s accurate. Messy or outdated data leads to bad decisions, no matter how fancy the AI model is.

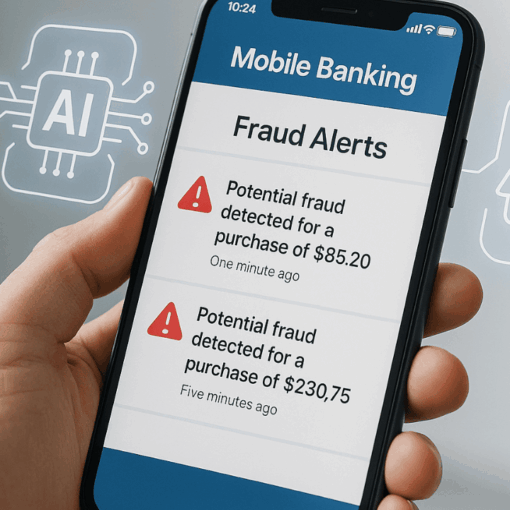

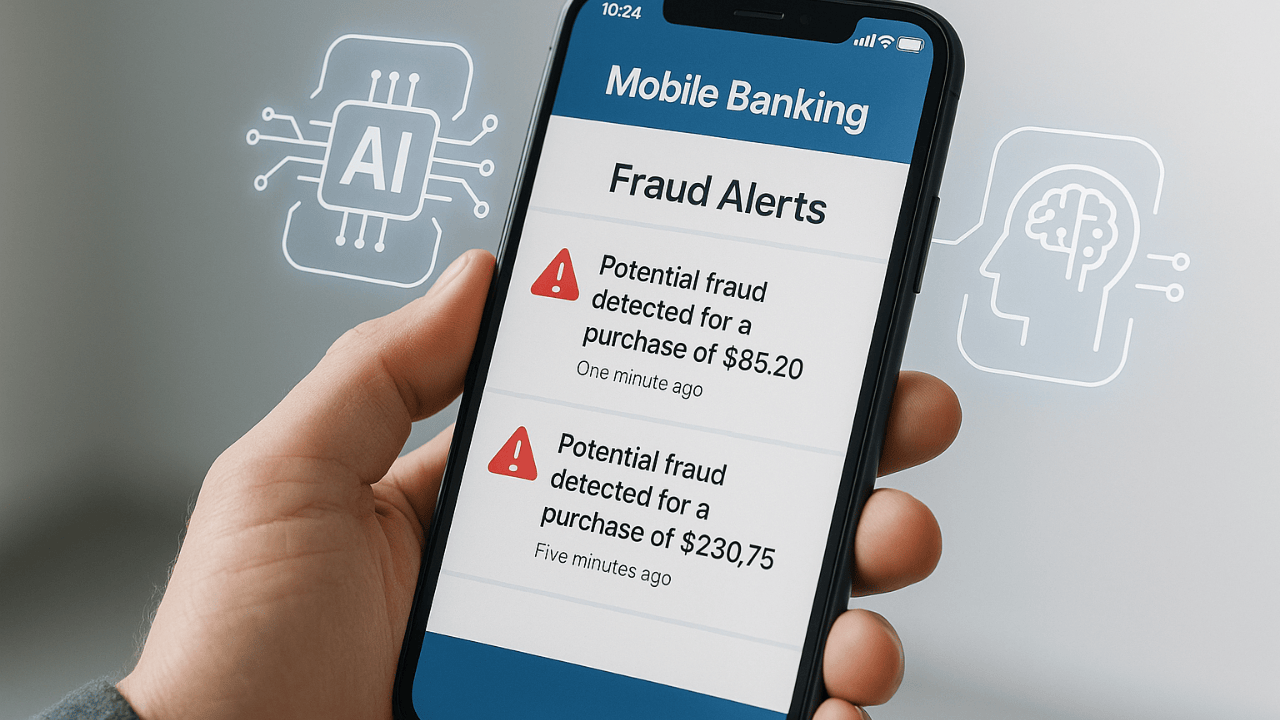

AI fraud detection works in real time

Fraud moves fast. So do smart systems that can spot it. With artificial intelligence in digital banking, banks can now track thousands of transactions per second and flag anything that looks off. These tools learn what normal looks like for each customer, then raise a red flag when something doesn’t fit the pattern.

Think of a debit card being used five times in five minutes in five different cities. Or a login from a new device at 3 a.m. followed by a wire transfer. These signals would take hours for a human team to spot, but AI can catch them in seconds.

The best part? It doesn’t slow down real customers. Older fraud systems often locked people out of their accounts or blocked cards for no reason. Modern AI tools get smarter over time, which means fewer false alarms and faster approvals.

Banks can also use AI to scan documents and applications. Tools like OCR and natural language processing check for fake IDs, altered bank statements, or stolen identities during the onboarding process. This cuts down on manual review time and keeps the bad guys out without creating more friction for good customers.

Community banks don’t have to run all this in-house. Many use cloud-based fraud tools that plug into their existing platforms. The goal is quick wins: fewer fraud losses and better customer trust without a long learning curve.

AI chatbots can actually be helpful now

A few years ago, banking chatbots weren’t great. They could answer basic questions but struggled with anything more. Today’s AI bots are miles ahead. They can help users reset passwords, check balances, make transfers, and even explain loan terms.

That means customers don’t have to wait on hold or stop by a branch to get help. Banks can offer support around the clock without hiring a night crew. And the bots are getting smarter by the day. They learn from each interaction and can hand things off to a human when needed.

Natural language processing lets these bots understand how people really talk. If someone types “I lost my card” or “Can I get a new debit,” the bot knows what to do. That feels a lot more natural than filling out a form or picking from a list of options.

This doesn’t mean people are getting replaced. AI handles the simple stuff so staff can focus on complex cases and relationship-building. When someone does call in or visit, bankers have more time to actually talk things through.

Banks that invest in good chatbot tech often see a drop in call volume and higher customer satisfaction. And because the bots can pull data in real time, they can offer personalized help, not just generic answers.

How community bankers can start smart

Jumping into artificial intelligence in digital banking doesn’t mean buying every new tool out there. For community banks, it’s about finding what works for their size, their staff, and their customers. Start with problems that need solving, not with buzzwords.

Most banks already have a lot of customer data. The first step is getting that data organized and usable. That might mean upgrading a core system or connecting platforms that don’t talk to each other. Clean, connected data is what fuels every useful AI tool.

Pick one use case to test. That could be a fraud detection add-on, a simple chatbot, or a loan recommendation engine. See what it does, how it works with your team, and whether it makes life better for customers.

Don’t forget training. AI doesn’t work on autopilot. Teams need to understand how it fits into daily operations and what to do when the system flags something. That’s especially true for compliance teams and frontline staff.

Finally, talk to customers. See what they like about digital banking and where they get stuck. AI should solve real problems, not just add bells and whistles. When banks focus on making things easier, faster, and more personal, the right tools become obvious.

Key Takeaways

Artificial intelligence in digital banking gives community banks a chance to do more with less. With smart personalization, predictive analytics, better fraud protection, and helpful AI chat, banks can meet the expectations of a digital-first world without losing the personal touch that sets them apart. The path forward starts with clean data, focused goals, and tools that fit real needs.

Contact Us to get expert help setting up the right AI tools for your bank’s digital future.

{kind=link}

{kind=link}

{kind=link}

{kind=link}